On March 22, 2012 I wrote an article about what I perceive to be a potential danger to investors: a dividend trap.

The premise of the article is simple: investors are starved of yield – by design of the Treasury and the Federal Reserve – and Wall Street knows it. So Wall Street will likely conspire to inflate yields to draw investors into stocks.

I pointed out that famed market guru Bruce Krasting noted a tendency of companies to pay dividends from debt.

He wrote: "These are referred to as Dividend Deals. The borrower takes on new debt in order to pay a stock dividend to common shareholders. (I prefer to see dividends paid from cash flow from operations, not new debt.)"

I then made a big and frankly pretty stupid mistake with reference to an example of such a company.

I talked about Seadrill (NYSE: SDRL) a deep sea driller that pays a substantial dividend with a high level of debt.

But I then incorrectly pointed out that Seadrill pays out MORE in dividends than it makes in earnings. I made a mistake of not really digging through the relevant SEC reports to double check my premise.

In hindsight using SDRL as an example of a debt funded dividend payer wasn't the right choice.

The metric I was looking at was the company's dividend payout ratio, which based on EPS looks tenuous at best. But as some readers have suggested, a look at cash flow suggests the dividend is more reliable.

One of the keys to Seadrill's dividend success in the future is that the debt to fund expansion of new rigs appears to promise continued growth and sustainable cash flows. This debt vs. growth conversation gets into a broader discussion than I had intended with the article so I won't get into the details.

But I do stand by my point that investors need to be wary about chasing yield and do their homework to understand where those dividends are coming from – my Seadrill faux-pas being just the latest relevant (and professionally embarrassing) example of how easy it is to make foolhardy assumptions about the relevant details.

So let my mistake serve as a lesson to really make sure a company can afford to sustain its dividend.

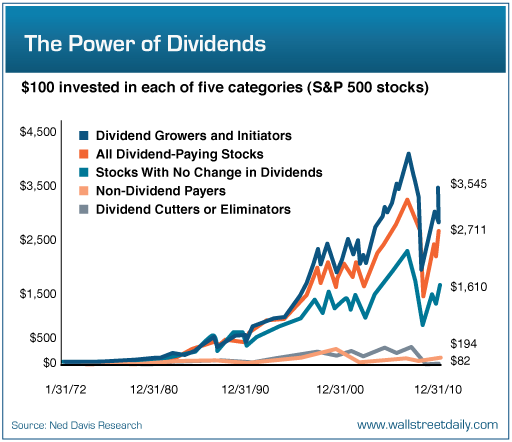

For a final warning of how dangerous it can be to chase yield, take a look at this chart plotting dividend cutters against other classifications of dividend companies:

Being the owner of a dividend cutter essentially means losing money over the long term. So you should avoid companies that have any potential whatsoever of cutting their dividend.

Be careful out there. It's easy to make mistakes. And they're usually expensive.

Have a great holiday,

Kevin McElroy

Editor

Resource Prospector Pro