Many investors are attracted to the hot market. I'm not one of them. The problem with the hot market is the "greater fool" aspect of investing becomes a larger variable in the equation. The likelihood of passing the investment up to someone else diminishes the longer the hot streak continues.

Rental residential real estate is a hot market. Nationally, rents are up 3% year-over-year, according to real estate information provider Zillow.com. Rents in many markets have moved up much more briskly. In Chicago and Minneapolis, rents have risen 9% year-over-year. San Francisco and Detroit have seen 5% year-over-year increases.

Supply, meanwhile, has dwindled down. Nationwide, the apartment vacancy rate has dropped to 5.2%, its lowest level in more than a decade, according to research firm Reis Inc.

Vacancies are even lower in many regions of the country, and not just in the tony burgs of Washington D.C., San Francisco, and New York. For instance, apartment vacancies in downtown Des Moines, Iowa are down to 2.1%.

There have been many positive articles on the rental market over the past year. One of the more insightful articles, titled "Why Renters Rule U.S. Housing Market," was posted by Gary Shilling on Bloomberg. Renter could hold the influence of buyers held six years ago.

Not surprising, the apartment REITs have moved up strongly over the past year. The bigger REITS have posted strong double-digit gains: Post Properties (NYSE: PPS) is up 28%, Essex Property Trust (NYSE: ESS) is up 22%, and AvalonBay Communities (NYSE: AVB) is up 18%.

These large apartment REITs have benefited from a frothy rental market, but there is no guarantee the froth will remain (and I don't think renters ruling the market like buyers is a good thing). Competition looms, and not just from other multi-family property developers.

Many individual investors are sopping up the glut of distressed single-family properties with the hope of turning them into rental gold. More rental supply will attenuate rent increases in the coming year.

I'm not so much concerned about rent as I am that apartment REITs simply aren't meeting their mandate – to provide investors with high-yield income. The aforementioned REITs yield less than 3%. Many other apartment REITs yield between 3% and 5%.

I see better income opportunities in other REIT sectors. What's more, I see stable growing income, unaccompanied by the gold-rush mentality that's driving prices in residential rental real estate.

The long-term care facilities REITs are particularly attractive: the sector has been relatively staid, yet the demographics are fantastic.

The U.S. Census Bureau reports there are 40.2 million Americans 65 and older, and they account for 13% of the U.S. population. That number is expected to expand to 88 million and account for 20% of the population by 2030, and remain at that elevated level going forward.

Treating and tending to the swelling ranks of the elderly will cost money, and a lot of it. The Congressional Budget Office (CBO) estimates that we will be spending $295 billion on long-term care by 2030. That's up from $160.7 billion today.

Nearly two-thirds of those 2030 dollars – $192 billion – will be spent on long-term care in an institutional setting, such as skilled-nursing and assisted-living facilities. That's more than triple the amount we spend today.

High Yield Wealth REIT Omega Healthcare Investors (NYSE: OHI) is an income investment well-positioned to exploit the developing real estate opportunities in long-term elderly care.

Omega maintains a diversified portfolio of 399 long-term care properties located in 35 states. Ninety-six percent of these facilities are dedicated to skilled nursing care, which cater to the needs of the chronically ill, most of them elderly.

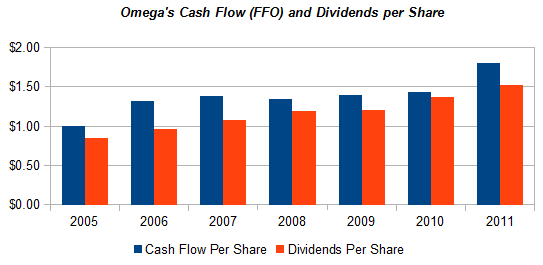

Omega has grown rapidly over the past decade. Since 2004, its facility count and revenue dollars have both trended continually higher. Seven years ago, Omega owned 221 facilities in 27 states. Those facilities generated $90 million in annual revenue. The 399 facilities Omega owns today generated $292 million in 2011 revenue. Revenue is expected to rise to $323 million this year and to $345 million in 2013.

With an ordinary publicly traded C-corporation, investors pay close attention to earnings. REITs are different. The focus is much more on cash flow, specifically funds from operations (FFO). FFO is similar to EBIDTA in that non-cash expenses, depreciation and amortization are added back to earnings.

As FFO goes, so go dividends. Both have moved higher over the years to the point where Omega yields close to 8%, making it one of the highest yielding investments among long-term care REITS.

The trend in FFO and dividends will likely continue. Management has a history of setting cash flow expectations, and then beating them. Back in August, management had expected Omega to generate FFO of $1.82-$1.86 per share. Three months later, in November, management upped guidance to $1.86-$1.88 per share.

After reporting fourth-quarter 2011 FFO of $0.50 per share, beating the consensus estimate by $0.03, management again raised FFO estimates. FFO is now expected to post between $2.06 and $2.12 per share for 2012.

Omega's stated policy is to pay at least 80% of its FFO in dividends. Last year, it paid 85%, the historical norm. Eighty-five percent applied to the mid-range of $2.09 points to a $1.77 dividend for 2012, nearly 8% higher than the current dividend rate of $1.64.

The $1.77 dividend is a reasonable (possibly low) expectation. Omega's dividend has been increased in four out of the five most recent quarters. The most recent quarterly dividend increase occurred in January, when it was raised 2.5%, to $0.41 per share.

Omega Healthcare Investors provides investors with a market-beating yield – 8% – generated in a REIT sector whose upward trend is sustainable for decades, much less years.