Yesterday we learned that new single-family home prices in the U.S.

have hit a five-year high.

The average new home will now set you back $256,000. That’s 11.2%

more than the same house would have cost a year ago, and the highest

level since March 2007.

If you’re in the market for an existing home, the average price is

$187,400, up 9.5% from a year ago.

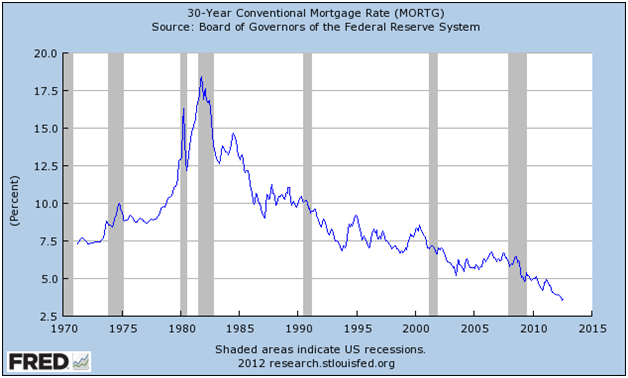

But despite rising prices, many prospective home buyers are still

anxious to close a deal while interest rates are at record lows, as this

chart of mortgage rates since the 1970s shows.

Yet interestingly enough, home prices are rising fast enough to

push overall housing affordability down from the highs posted earlier in

the year.

The most recent reading from the National Association of

Homebuyer’s Housing Affordability Index was at the end of the second

quarter of 2012, and came in at 185.1. That’s down from 205.2 at the end

of the first quarter, and also below the level of 197 posted at the end

of 2011.

In order to bring this index back to record levels, prices or

interest rates need to drop.

Interest rates pose a more interesting discussion in the wake of

QE3. After all, one would think that the Fed’s plan to purchase $40

million of mortgage-backed securities each month would help push rates

lower – maybe even below 3%.

But not so fast. The average 30-year fixed rate is still around

3.6%.

Yes, that’s a bargain compared to 4.1% a year ago and 5.0% two

years ago. But the mortgage industry can do better. It just doesn’t

appear to want to.

An interesting piece in The New York Times last week

suggested that the spread banks make on mortgages right now are wider

than a year ago, despite the lower interest rates.

This spread is essentially the difference between the interest rate

on a mortgage and the rate the bank earns when it sells that same loan,

which is packaged into government guaranteed mortgage-backed

bonds.

According to the article, the average spread since 2007 has been

around 0.77%. In September 2011, it was 0.74%.

But right now? This spread appears to be more than 1.4%. That means

a 30-year fixed mortgage could theoretically be locked in at around 2.8%

and the industry would enjoy the same profit it made in the four or so

years after the housing bust.

If that were the case, housing affordability would likely push back

above the record high that it reached at the end of the second quarter,

even if home prices continued to rise moderately.

But while any consumer would love a 30-year fixed mortgage below

3.0%, I don’t recommend holding your breath.

It’s far better for homebuyers to buy the right home and strike

that perfect balance between principal and interest payments each month.

That means saving for a nice downpayment to begin with, and buying a

house that is well within their means.

The lower the principal, the lower the interest payment and the

lower the overall cost of home ownership over the long-term. And that

means more equity is built up in the actual property over time. If

property values continue to climb – even slower than the double digit

rate over the last year – then buyers have still made a great investment

while also enjoying the utility of the home.

So while most of us would love to lock in the 3.0% 30-year fixed

mortgage that the industry appears to be able to afford, my advice is

find a house that you can make nice fat principal payments toward each

month.