The easiest way to be a successful commodity investor is to buy physical gold bullion and hold it until the end of this currency crisis.

But assuming you already own “enough” gold, you might be interested in another way to safely put money to work in the commodity sector.

So today I’d like to talk about one easy way that anyone can (and should) invest in commodities.

I’m talking about Dividend Reinvestment Plans or DRIPs.

You’ve probably heard of DRIPs – and you might even own some.

But not all DRIPs are the same. The whole idea of owning DRIPs is that it’s a low-cost way to accumulate shares – and to compound your dividend payments.

But many – in fact, most – DRIPs include a bunch of hidden fees, which can cut into your compounding rate as easily as a fee from a broker or a mutual fund.

The secret that most people miss out on is that there are plenty of great companies that offer NO-FEE or very low-fee plans.

Before I reveal two different companies and their plans, I’d like to briefly mention that many brokerages offer their own DRIPs of differing cost and availability. Depending on your brokerage, you MAY be able to enroll in any DRIP without paying fees. Talk to your broker, and make sure you ask about all of the details – like, is there a fee to reinvestment dividends? Is there a fee to enroll in a DRIP? Are there any processing fees, or fees to buy more shares?

In any event, I’d like to discuss a DRIP for one of my favorite oil companies, Chevron (NYSE: CVX), and compare it to another one of my favorite oil companies, Exxon-Mobil (NYSE: XOM).

Both of these companies currently trade for under 10 times earnings, which is a pretty low price to pay historically. And both of these companies pay dividends of over 2.5% with a solid history of raising their dividend.

Good place to start, right?

And at first blush, you might be inclined to enroll in the company with the highest current dividend yield.

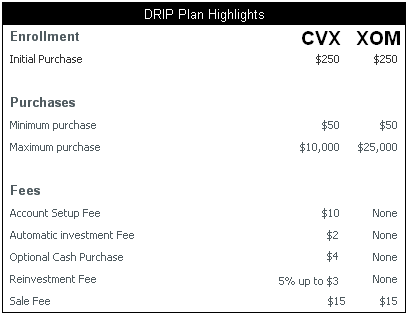

But the DRIP for Exxon, which has a trailing annual dividend yield of 2.8% has significantly lower fees than Chevron’s DRIP.

Look at their fee structures, side to side:

(hat tip to dripadvice.com for this graphic)

Even though Chevron’s dividend is higher right now, you get dinged at every possible angle with the Chevron plan. For someone starting out, the Exxon DRIP is a better choice – otherwise you’ll be paying through the nose for every new stock purchase, reinvestment and transaction.

For Exxon’s DRIP, the only fee you pay is when you sell. And why would you sell your DRIP? The whole idea is to hold it forever until your dividend payments are enough to live off of.

Over a 10 year period, you’d pay close to an additional $500 with the Chevron plan over the Exxon plan, assuming you bought shares regularly and reinvested all of your dividends.

Unless you’re initial investment is $5,000 or greater, you’d be better off with the Exxon plan.

That’s because Chevron’s dividend is only 0.9% bigger than Exxon’s.

A 0.9% difference only amounts to about $450 in extra income over that same 10 year time frame – all of which will get eaten up by the extra fees Chevron includes in their plan.

That’s the kind of information you need to be aware of – because not all DRIPs are created equal.

If you’re looking for more information on these types of no-fee DRIPs – check out a short write-up we completed on the subject.