We’ve talked in the past about trades that are too

one-sided. We’ve seen the U.S. dollar rally when everyone was looking for

it to collapse. We’ve seen housing stocks rally in a dead housing

market.

And most recently, we’ve seen bond yields rally in

the face of a Fed policy that was supposed to keep yields

contained.

Are we seeing the market repudiate the Fed’s

Treasury buying program? Are higher yields a statement that inflation is

on the way?

There are plenty of analysts and economists that

think QE2 is a bad idea. I’ve been one of them.

And even now, as economic data improves to the point

that GDP forecasts are moving higher, the Fed appears steadfast that the

economy needs more stimulus. The language in yesterday’s FOMC statement

was unchanged.

The inflationary risks of QE2 have been well

articulated by the anti-Fed crowd. And even though today’s CPI number

shows that inflation is not happening, it’s easy to interpret the rise in

bond yields as sign that inflation is right around the corner.

If employment picks up, inflation may become a risk.

But until that happens, there’s another way to interpret the rise in bond

yields: maybe yields are rising simply because investors are selling

bonds

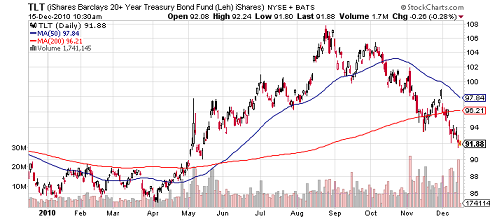

Here’s a one-year chart that shows the yield of the

10-year Treasury. It’s made a big move since early November. But let’s

look at the action for the 20+ Treasury bond ETF, TLT.

It’s pretty hard to miss the huge volume surge that

started in November, when the Fed actually announced its QE2

plans.

At its most simple level, a market is made of buyers

and sellers. When there are more sellers, prices fall. In the case of

bonds, more sellers means prices fall and yields rise. Maybe this is a

good time to think of bonds in terms of buyers and sellers, rather than

inflation.

Here’s a headline from Seeking Alpha, a popular

investment website: