Investing is not about "analysis" or timing or research or even about being lucky enough to buy the right assets at the right time.

Before you pick up a book about value investing or how to read a chart, first you need to learn about managing risk. If you don't understand risk, then every investment you make becomes a spin of the roulette wheel.

While you might not want to hear it, it's your job to manage risk. No one else can do it for you.

It is up to you, the self-directed investor, to make the ultimate decision on how to properly manage your investments. No one cares about your money more than you. So why do most investors choose not to properly hedge your portfolios?

You spend countless hours making money so that you can build a nest egg, yet most of you will not take the time to learn how to keep that same hard-earned money. Sadly, most of you spend more time watching the talking heads on CNBC hoping to pick up a stock tip or two.

Stop! Enough is enough. Did you not learn from the tech bubble, real-estate bubble or the latest euro crisis that the talking heads do not have the answers? They have an agenda and it's called ratings. They report what's sexy. What I am about to tell you is not sexy — it's far from it. But I don't care because my goal is to teach a few of you, who are truly interested, how to keep your money by using sound, realistic options strategies like credit spreads.

Hopefully I can give you a push in the right direction. I am not here to tell you what to invest in; rather, I want to teach you appropriate strategies.

If you are fearful of a sharp decline over the coming months, or think we are in for a sideways to slightly higher market and you want to keep your buy and hold portfolio intact, then I can teach you a few strategies that might soften the blow to your long-term portfolio.

While there are various ways to protect your portfolio using options (collars, protective puts), my favorite way is to use credit spreads.

I typically prefer to use credit spreads as my choice of hedging strategies because it allows me to take advantage of heightened fear in the market.

By selling credit spreads I can create a directional strategy on my assumptions – in this case, where I think the market is headed over the next 30 to 50 days – with limited risk and limited reward.

But more importantly, my assumptions do not have to be perfect or even right.

That's because credit spreads, while directional, allow for a margin of error.

Let me explain…

Let's say we are bearish on the market, so we want to sell a few bear call spreads on the SPDR S&P 500 (NYSE: SPY). SPY is the most liquid ETF as seen by the tight bid-ask spreads in the options chain below. An ETF or stock with highly liquid options is a necessity if you want to trade options effectively over the long term.

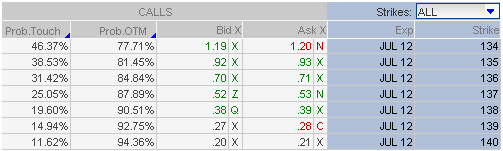

The first thing we want to do is choose our probability of success by looking at the options chain for SPY. With SPY trading at $128.05, I prefer to find something several strikes out of the money with a probability of success around 80%.

By looking at the delta or "probability of expiring out-of the-money" for SPY, we can simultaneously sell the July 2012 136 strike for $0.70 for a probability of success of roughly 85% (the likelihood that the 136 call will expire worthless and we will receive our max profit) and buy the July 2012 138 strike for $0.39. This would bring in a net credit of $0.31.

Let's see what this looks like on the chart. Basically, SPY could move 6.3% higher, stay the same, or move lower and the trade would make 18.3% (return is calculated based on the credit of $0.31 divided by the required margin of $1.69). Not a bad trade, considering the probability of success on the trade is roughly 85%.

So, basically if SPY remains below the bottom blue line the 136/138 credit spread will make 18.3%. Moreover, you would only take a max loss on the trade if SPY pushed above the blue line at 138.

Credit spreads are a great way to hedge your portfolio if you are indeed bearish. More specifically bear call spreads can be profitable even if the underlying stock moves higher. In this case the S&P 500 can move 6.3% and you would still make a nice gain.

Again, this is just one of many options strategies that offer a hedge for your overall portfolio.

If you would like to learn more about how I use options in a logical, mathematical way sign-up for my free newsletter The Strike Price. You will find valuable information on options selling strategies and more importantly, how to effectively use options within your portfolio.

Remember, feel free to email me at [email protected] with any questions that you might have regarding anything options. I am more than happy to help you learn what I feel is one of the most powerful options strategies available to self-directed investors.