Don’t let yesterday’s 110% rally in shares of Leap Wireless (NASDAQ:LEAP) entice you into investing in takeover targets to earn big returns.

Despite the huge premium AT&T (NYSE:T) has offered to pay with its $1.2 billion bid for Leap, it’s likely that speculating purely on takeover potential will be a losing bet.

You’re far better off investing in a company because you see catalysts to unlock growth or value in the company than solely on takeover hopes. Yes, takeover potential can factor into the equation, but you’ll want far more than that to go on if you expect to consistently earn big returns in stocks.

Part of the reason M&A is so difficult to anticipate is that there are so many factors involved in any given deal.

Getting the timing right is the most daunting challenge. You could end up sitting on a position that goes nowhere while awaiting a bid that never comes.

And while Leap’s proposed deal comes on the heels of several other acquisitions in the U.S. wireless space, the broader M&A industry is still relatively slow.

Earlier in the year there were a few megadeals which gave a temporary boost to the market, including the Berkshire Hathaway (NYSE:BRK-A) $28 billion takeover of H.J. Heinz Company (NYSE:HNZ) and the Liberty Global (NASDAQ: LBTYA) $23.3 billion takeover of Virgin Media (NASDAQ:VMED).

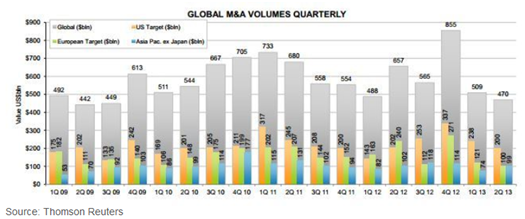

But despite these high profile deals, overall deal flow is extremely slow. Recent data from Thomson Reuters shows that global M&A activity through the first half of 2013 is weaker than at any time since Q4 2009, and has fallen 9.0% year-over-year.

You might think that in a market where companies appear to be growing there are ample opportunities for acquiring companies to unlock value by snatching up smaller players.

However, with many stocks at all time highs there are fewer “deep values” out there. That raises the stakes of any takeover deal.

Low interest rates have also played more of a factor than many Main Street investors realize.

One of the consequences of the low interest rate environment over the last few years has been cheap financing in the high-yield bond market, a key funding source for M&A and leveraged buyouts (LBO).

That meant some potential buyout candidates were been able to issue bonds at low rates, near 5%, up until this past May. They avoided outright sale in favor of leveraging up with inexpensive debt, thereby staying independent.

Now, high-yield bonds are rising after Bernanke has hinted that the Fed’s quantitative easing programs may begin to wind down soon.

And that has created another challenge for M&A activity – volatility.

High-Yield bond yields have recently surged from 5% to nearly 7%, a 40% increase in just a few months.

That volatility dramatically changes the terms of any potential debt-funded deal, both for companies looking to sell and for companies looking to buy.

And equally important, the incentive to wait until interest rate volatility simmers down is much higher.

In a world where the cost of capital governs most decisions – whether explicitly or implicitly – it stands to reason that the M&A market won’t start moving and shaking again until there is more certainty surrounding interest rates.

Money to fund deals always comes at a cost. And until those costs are more predictable, don’t expect deal flow to pick up.

Your best bet is to invest in companies based on their own merits, not on any potential – rumored or real – to be bought out.

If a takeover occurs, as it did for Leap Wireless, then that’s great. But in this market I recommend you have more catalysts factored into your investment thesis than just takeover speculation.

Good Investing,

Tyler Laundon, MBA