-

Three assumptions

about money -

Gold vs. Treasures

– what’s more overbought? -

A Ten-Fold

difference

There’s been lots of chatter

about a gold bubble. But I think you can make a much stronger argument that

Treasuries are in the midst of history’s biggest bubble right

now.

Let me back up, because I know I’m making some short-cut assumptions that

you might not make for yourself.

1) I’m assuming that gold IS

money. That is, it’s a store of value and a medium of exchange.

2) I’m assuming that the

definition of a bubble describes when an asset is overbought to the point

that its price is much, much higher than it should be.

3) If I can safely make these

assumptions, then I think it’s fair to compare gold to another form of money:

the dollar, and by proxy U.S. Treasuries.

If we can agree that U.S.

Treasuries are a fair proxy for the dollar, and that gold is money – then I

truly struggle to see how ANYONE can come to the conclusion that gold is in a

bubble, while simultaneously seeing Treasuries as not being in a

bubble.

Here’s why:

In 2009 the total amount of gold mined, from every mine, in every country

for the whole year amounted to $90.6 billion. That was about 90 metric tons

more – or a little under $3.5 billion – than the amount mined in 2008. If

you’re keeping score, I’m using gold at $1,200 an ounce as my price

point.

That $90.6 billion includes

all gold for electronics, jewelry and bullion.

According to the 2008 US

Geological Survey, less than 10% of all gold is turned into bullion – most of

it becomes jewelry, or is used in dental or medical services.

So it’s safe to say that only

about $9 billion worth of gold was turned into bullion last year – maybe a

little more, but not much. The U.S. mint only minted about $1.7 billion worth

of gold into gold eagles, buffaloes, etc.

So, let’s round it up to an

even $10 billion worth of gold bullion sold last year. That’s small potatoes,

really.

Forbes magazine publishes an annual list of a few dozen billionaires who

could each buy all of the world’s annual bullion production.

Our Federal government actually loses more than twice that every

year.

So $10 billion seems like a

drip in the ocean.

In any event, that $90.6

billion of new gold in world circulation is still a tiny number, especially

when you compare it to the amount of money going into US Treasuries

today.

A recent article in

Business Week reminded me of the size of the Treasury

market:

“The government will

auction $69 billion of the maturities next week, according to the median

forecast in the survey, compared with $70 billion last month and a

record-tying $81 billion in February.”

So at the current sales pace, the U.S. Treasury will sell at least 10 times

more Treasury notes than the total amount of gold produced this year. But

that’s just U.S. bonds – it doesn’t account for any debt sold out of the

Euro-zone, or Asia, South America, Africa, or Australia – which is nothing to

sneeze at.

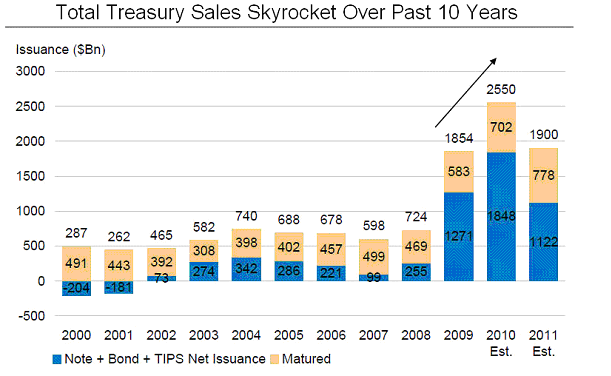

Click on this chart below for

the full-size version, to see how US Treasury sales have ballooned over the

past 10 years:

Meanwhile, gold production (and sales) has stayed relatively

flat:

Total Gold Production In Metric Tons (2003-2009)

|

2003 |

2004 |

2005 |

2006 |

2007 |

2008 |

2009 |

|

2,420 |

2,470 |

2,370 |

2,370 |

2,280 |

2,260 |

2,350 |

Right now, Treasuries are still selling near their record

high prices. The yields are near all time lows. There’s huge demand for

Treasuries, and both in volume of sales as well as growth of sales,

Treasuries dwarf gold.

If you’re eschewing gold, but buying Treasuries (especially

long-term Treasuries) I’ve got to wonder about the thought process –

especially as more and more sovereign debt issues spring up across the pond.

Today Portugal’s debt just got downgraded, and if you think the Atlantic

ocean will protect us from the same exact problems, then I guess you should

keep buying Treasuries.

It’s worked so far.

Drop me a line if you feel inclined to set me straight:

[email protected].

Good Investing,

Kevin McElroy

Editor

Resource Prospector