As you know, I’m a firm believer that oil prices are among the best

indicators for the stock market. When oil prices rise, stocks do too. It’s

because they both react to the same catalyst: expectations about future

growth.

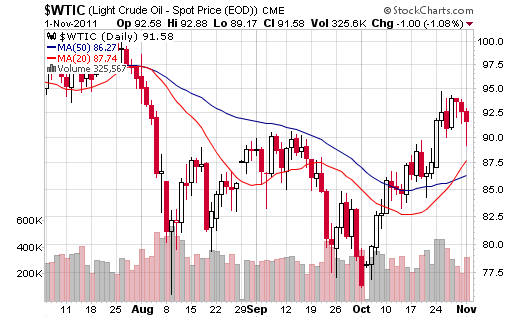

Over the last few days, I’ve advised readers to watch the $90 a barrel

level for oil. A break below $90 is a sign that investors are worried about

future growth.

We saw this clearly in late summer. Oil began its decline after the

disastrous Durable Goods report from July 28.

The inability to break above $90 in September was a good indicator that new

lows were coming. And sure enough, as the talk of a double-dip recession

reached a crescendo, oil was trading down into the upper-$70s.

Yesterday, after the semi-positive employment news, oil pushed higher as

investors anticipated steady growth at the very least.

More telling to me, though, was the recovery from sub-$90 on Tuesday. That

show of strength was not reflected in the stock market. In fact, the

S&P 500 closed at its lows of the day.

Why did oil move higher? Couldn’t we just get a read on the stock market?

Or use gold as an indicator?

Oil is more useful as an indicator than even stocks because of one thing:

business. Many businesses use oil futures to hedge their operating costs

and lock in supply. Airlines and shipping/trucking, for instance, are

better economic indicators than Apple (Nasdaq:AAPL).

Stocks, along with gold, are far too dependent on the whims of investors to

be a reliable indicator.

Right now, oil looks more bearish than bullish. And how it reacts to

Friday’s Nonfarm payroll number could set the stage for the next big move

for stocks.

The Fed’s latest FOMC meeting yielded no changes to the statement.

“Significant downside risks” remain, though growth has improved.

Of course, what exactly the Fed means by “significant risks” isn’t spelled

out. We can assume Europe, or the high unemployment rate. But I’d say it’s

a rhetorical statement that allows the Fed to keep Operation Twist going

and leaves the threat of QE3 on the table.

Why do I call QE3 a threat? Because like it or not, the Fed sees the stock

market as part of the key to economic recovery. If it can maintain some

underlying strength in stocks by keeping shorts at bay with the threat of a

liquidity-driven rally, it will.

A majority of economists believe that QE3 is coming at some point next

year. I’m not so sure. The Fed can accomplish a lot just by keeping QE3 on

the table. Of course, if growth takes a nosedive, or interest rates move

higher, the Fed will act.

But those are the only scenarios (outside of some economic shock) I see

that will prompt the Fed. And because I believe the economy will stumble

along, I don’t think the Fed acts.

Write me anytime at [email protected]

Ian Wyatt

Editor

Daily Profit