As part of my continued series on this world-gone-mad – I’d like to point out a commodity trend that simply doesn’t make any sense.

For decades and in fact, for almost the entire history of the American stock market, commodities and the Dow Jones Industrial Average Index moved inversely to each other.

In other words, when stocks go up, commodities usually go down.

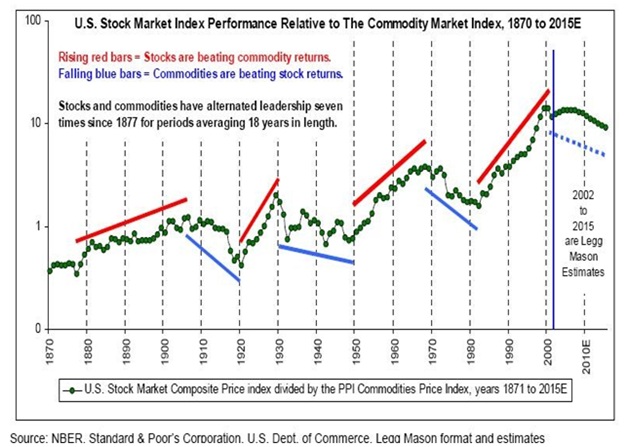

You’ve probably seen this chart – which shows the inverse relationship:

I’ve posted this chart probably a dozen times in the past few years.

And while it’s somewhat out of date – until the past 18 months or so, this inverse trend between stocks and commodities was still pretty accurate.

But something happened over the last few years that has coupled nearly every asset together. Almost everything is correlated.

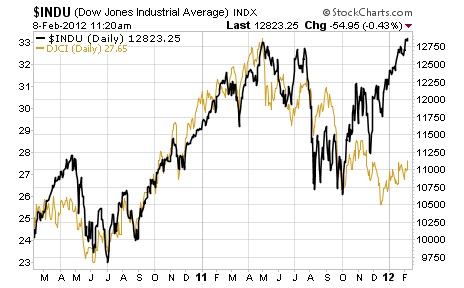

Here’s the Dow again, charted alongside a commodity index for the past 2 years:

That’s pretty remarkable correlation over a significant amount of time.

So you have to ask yourself why? Why are commodities and stocks synced up like they haven’t ever been before?

The simple answer is that we’re not living in normal times. The Federal Reserve and European Central banks have so decoupled prices from any kind of normal market pressure that all assets trade not in relation to each other, but rather, they trade with regard to currency movements.

The conclusion we should draw from this bizarre market behavior should be mixed with lots of cautious optimism for commodities.

Yes – the dollar index has more control over commodities than any real market pressures.

But that situation isn’t likely to last forever – and all of the funny-money business that central bankers have been engaged in should be long-term bullish for commodities.

Money printing (or quantitative easing or whatever you want to call it) is good for gold, silver, oil, coal, etc.

It might be bad for stocks.

But that’s okay. That’s why I’m heavily invested in commodities and why I’ve kept my stock exposure minimal.

When we come back through the looking glass, into the real world, the pent up pressures between commodities and stocks should reward commodities.