-

Don’t forget about the

railroads -

Three railroads that transport most of our

coal - 112% average gains since 1999

Are you sick of hearing about a double-dip recession

yet? There seems to be a consensus that the recession is back, or almost

back – and although I do so without relish, I happen to agree.

It’s this kind of investment atmosphere that makes me

want to crawl back to the basics. And nothing is more basic and important

than coal. In the United States we get about half of our electricity

generation from coal. China, the #1 largest consumer of coal gets about

70% of its electricity from coal.

Every time I

mention coal, my wife inevitably gets a phone call from my father-in-law

Ron, telling her to remind me, “Don’t forget about the railroads.”

And he’s right, the railroads are vital to transport

coal from mines to population centers.

According to the Energy

Information Administration the railroads account for 64% of all

domestic coal shipments in the U.S.

I don’t know how bad this double dip recession will be,

or how long the secular bear market will continue – but I’m sure that no

matter how bad or long, we will continue to use coal to generate

electricity AND that trains will transport that coal. The best part is,

even if I’m wrong, and we’re not entering a double-dip recession, and the

12 year secular bear market is over – we’ll probably use even more

coal!

And to take advantage of this rock-solid trend, there

are only three companies you need to think about.

That’s because only three publicly traded railroads

supply the majority of coal transportation in the United States.

If you live on the East coast, you can be fairly sure

that the coal currently keeping your lights on gets delivered by one of

two railroads: CSX Transportation (NYSE: CSX) or Norfolk

Southern Corp. (NYSE: NSC).

Most West coast coal gets moved by either Union Pacific

(NYSE: UNP) or recent Warren Buffett acquisition

Burlington Northern Santa Fe, which is no longer publicly traded.

These three railroads have been bear market super-stars,

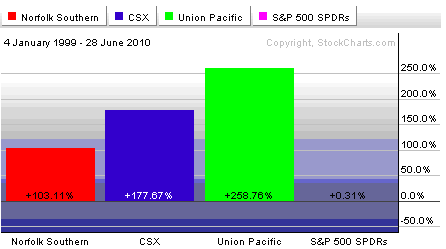

and I don’t expect that to change anytime soon. The chart below shows the

gains made for all three companies vs. the S&P 500 from January 1999

to today:

I have to admit, even I was a little shocked at how well

these boring large-cap grey-chip companies seem to have the gains of

high-growth micro-caps. That’s an average gain of 112% for these three

companies, compared to…zero for the broad market since January of

1999.

So these companies obviously have a great deal of value.

They provide the majority of coal used for electricity generation in this

country. That’s tough to quantify. All three of these companies trade

between 17-19 times trailing earnings, so they’re not extraordinarily

cheap, nor are they extremely expensive.

Benjamin Graham always talked about how he didn’t like

to pay more than 16 times earnings. The good news is that projected

forward PE for all of these companies is in the mid-12 range.

If you’re interested in owning these companies (and you

should be) I’d look to build a position slowly by averaging in, as

always.

Union Pacific is the largest of these companies with a

market cap of just under $45 billion. The stock currently sells for about

$72.60, and I’d look for any opportunity to buy this company under $70.

If it gets whacked during the double dip, I’d gladly buy more under $60.

This company pays a 1.8% dividend.

Norfolk Southern has a market

cap of $20 billion, and currently sells for around $55. The company is a

screaming buy under $50, but could dip below $40 on broad market

weakness. It pays a 2.4% dividend right now.

CSX’s market cap is a hair under $20 billion right now,

and the stock is selling for about $51. Load up if shares drop below $45.

The company also pays a 1.8% dividend.

I really like these companies as long term plays on coal

demand. Coal isn’t going anywhere, and neither are these companies. They

all have double-digit profit margins – meaning they have a good cushion

of profitability if the economy gets bad. They can lower prices and still

make money. And since they’re essentially monopolies on coal

transportation, they can probably raise prices pretty easily as

well.

I’ve run out of room in today’s issue, but if you’re

interested in learning about a Chinese coal company that’s ideally

situated in China’s centuries old “silk road” region, you can

click here to read a full write up.

Good investing,

Kevin McElroy

Editor

Resource Prospector