-

The indicator is flashing right

now - How to compare apples to apples

- The investment to buy today

Seven months ago, this indicator flashed telling me that it

was time to buy one specific energy commodity above all others. I recommended

buying one simple investment to take advantage of the impending

uptrend.

If you bought that investment then, you’d currently be

sitting on a 25% gain and you would have collected an additional 4.2% in

dividends.

The good news is

that this indicator is flashing AGAIN, and I believe that if you buy this

investment now, you’ll be in a good position to capture similar gains over

the next 6-9 months.

What am I talking about?

Well, on April 5, 2010 I wrote to you saying it was time to

buy natural gas. Natural gas had just bounced off of year-to-date lows just

under $4 per thousand-cubic-feet (MCF).

But more importantly, natural gas was selling near all-time

record lows when compared to the price of oil. I like to compare resource to

resource – because I’m not a currency expert. I don’t really think anyone is

– I mean, how could anyone accurately tell you what a Federal Reserve note is

worth?

It’s nearly

impossible to guess what one dollar will be worth a week from now, let alone

a month or a year. So it’s much more useful and helpful to look at an

apples-to-apples comparison.

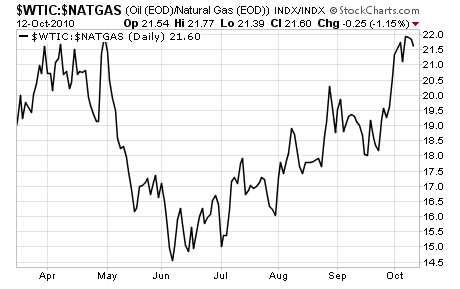

So I compare natural gas prices to oil prices.

That’s the indicator I’ve been referring to. I simply take

the cost of one barrel of oil, and divide it by the cost of one MCF of

natural gas.

Last April, the ratio was making new all-time highs, and

today, it’s again scratching into new territory.

I believe that this ratio will again drop back to more

‘normal’ levels below a ratio of 20 – and when it does, my favorite natural

gas dividend payer should rise.

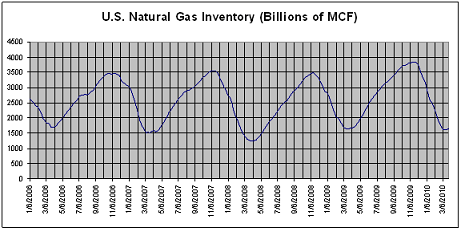

The other reason I’m excited about natural gas prices is

that inventories this time of year are typically near all-time highs. This

year is no different.

I’ve plotted the five year inventories to show the very

predictable nature of natural gas in this country:

You can see how the September-November range is when

inventories are building and reaching their peak. It’s not surprising to see

annual lows for natural gas prices this time of year for that reason. Lots of

excess inventory (supply) easily satisfies demand, so prices remain

low.

But as the weather gets colder, we’ll burn natural gas to

heat our homes, inventory will fall, and prices should rise.

It’s possible that natural gas prices could fall – but it’s

not likely. And as they rise over the next few months, there’s one company

that should benefit.

I’m talking about

Hugoton Royalty Trust (NYSE: HGT). If you’ve been a reader

for very long, you probably remember me bragging about the gains you could be

enjoying if you had bought this stock back in April when I first recommended

it.

The good news is that I think this company is again a

compelling buy. The bad news is that it likely won’t stay that way for

long.

This company owns royalty stakes in several natural gas

properties in the United States. It’s pretty simple: it gets paid a cut of

the profits from the natural gas that these producers bring to market. That’s

it! It has no other assets besides the cash it gets from these producers. And

it has zero debt!

And the best part: Hugoton currently pays a 7.9%

dividend.

The business couldn’t be simpler.

Like I said, this stock isn’t likely to be a good buy for

very long.

I’d recommend picking up shares UNDER $21. That price has

been a resistance point for months now, so don’t chase.

Good investing,

Kevin McElroy

Editor

Resource Prospector

full disclosure: As of this publication date, I own no shares of

Hugoton