- One thing to keep in mind…

- The pirate premium

- A 10.8% dividend

Yesterday I discussed the overwhelming importance of oil and its

implications for your investments.

My most important advice in yesterday’s issue was buried

down at the bottom, so you might have missed it. Here it is to recap:

“if

I can leave

you with one thing to keep in mind, it’s to remember the importance of oil –

even for non-commodity investments. You need to look at all of your

investments, from stocks even down to bonds and savings accounts, and think

about how oil price fluctuations could affect the bottom line of the

underlying assets and businesses you’re invested in.”

I also promised that I would look into some specific oil

investments to buy under the assumption that the recession has resumed or is

on the horizon.

During a recession, oil prices tend to sag due to decreased

demand for oil, which doesn’t usually bode well for most types of oil

companies.

Sure, a company like Exxon (NYSE: XOM) is

hedged 20 different ways for just about every market climate, so they won’t

get too shellacked during a sustained recession. But I’ve banged the gavel

enough on Exxon, and if you’re not convinced to own it yet, there’s not

really much more I can say. Okay, one more thing: Exxon is

still cheaper than it was during anytime in

2009.

Moving on to slightly different, and just about as green

pastures, I’ve long admired the business structure of oil shipper

companies.

These companies typically negotiate a set rate dependent

upon a variety of factors largely independent of oil prices. So, while they

might have to contend with weather, pirates, port fees, licensing and a

variety of maritime laws, they’re usually compensated on the basis of largely

predetermined factors within those categories. What they don’t have to worry

about as much is the price of their cargo.

Let me give a quick example of what I’m talking

about.

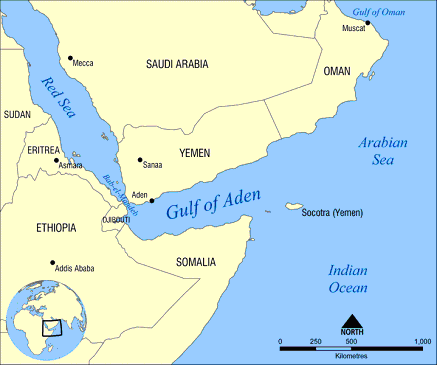

You might remember

last year when Somali pirates were making big news for capturing ships in and

around the Gulf of Aden.

The Gulf of Aden is a choke-point for all shipping traffic

back and forth between the Mediterranean Sea to East Africa, India, many

parts of Asia, and Australia.

Here’s a map that shows the proximity of the shipping lanes

to Somalia:

Companies shipping goods through this area were basically

paid a “pirate premium” for the excess risk involved in doing business

through the Gulf of Aden.

That premium has nothing to do with the price of the goods

on board, it’s a straight multiplier determined by shipping

authorities.

One such company Nordic American Tanker (NYSE:

NAT) had some of the newest, fastest, most pirate proof ships in

that area, so even though there was little chance they’d get nabbed, they

still collected the premium.

And shares of NAT did quite well during the height of pirate

paranoia in March-June 2009.

Shares appreciated 50% in two months.

Companies like NAT can benefit, even while the price of oil

is falling or stagnant – because even if we’re in a bad recession, we’re

still going to use plenty of oil.

I wouldn’t suggest

buying NAT today – but another oil shipping company has caught my eye:

Teekay Tankers (NYSE: TNK).

I like this company as a recession play for two

reasons:

About half of its ships are under pre-negotiated shipping

contracts, so it has a bit of a built in safety-net.

It pays a large dividend, and has done so for the entire

history of its company. Today TNK pays a 10.8% dividend, which is the kind of

income that will make it easier to ignore daily price fluctuations.

If you’ve been looking for a way to invest in oil, and

protect yourself from a recession, then this oil services income play might

be a good place to look.

Good investing,

Kevin McElroy

Editor

Resource Prospector

disclosure: no positions