Lydia H. had a problem. So did Liz R., Rene C. and Nansee K. Their problem was not all that unusual. In fact, their problem was one facing many people today: Banks refused to extend them credit.

And why should banks extend credit? Did you know that the Federal Reserve is actually paying banks to sit on loanable reserves? It’s true – the Emergency Economic Stabilization Act of 2008 allows the Fed to pay interest on "excess reserves" that U.S. banks park at the Fed.

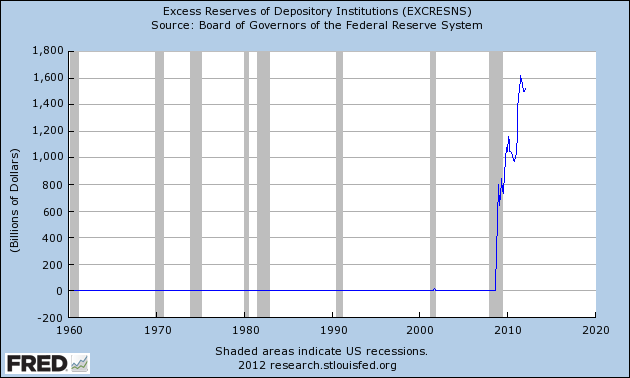

Forget about lending to the rest of us so we can start a business, buy a home, or consolidate debt. No, today banks can just send their cash to the Fed and watch the money accumulate risk-free. If you think I’m exaggerating, take a look at the graph below. In 2008, excess reserves parked at the Fed spiked to $1.6 trillion from zero, where it had been for the past 48 years.

The Fed’s bank-subsidizing policies have not only harmed borrowers, they have harmed investors and savers as well. Banks offer a paltry 25 basis points on passbook savings accounts and a mere 70 basis points on a six-month certificate of deposit (CD). If you’re willing to tie up your money for half a decade, banks will "generously" offer you 1.75% annually on a five-year CD.

Thankfully, we can count on markets and entrepreneurs to bypass the banks parsimonious ways and solve problems government officials and banks can’t or won’t solve . or deliberately exacerbate.

Lydia, Liz, Rene, and Nansee needed money; investors needed income and yield. Why not put the two groups together while rendering the banks and the Federal Reserve irrelevant? The borrowers get the money they need (often at better terms than the banks offer) and the investors – acting as lenders – generate superior income and return on their money.

That’s what’s occurring today, thanks to the burgeoning peer-to-peer lending market – where individual investors (lenders) are earning 6%, 10%, 15%, and even 18% on their money annually.

Becoming a peer-to-peer lender is easy and readily accessible to most investors, regardless of their level of financial sophistication. You don’t have to be an expert in credit analysis to lend.

The peer-to-peer market makers do all the heavy lifting. They vet the borrowers and monitor them to ensure they pay principle and interest in monthly installments. Missed payments lead to penalties, because the peer-to-peer market makers report non-payers to credit agencies and send accounts to collection agencies just as any bank would.

Prosper.com and LendingClub.com are the premier peer-to-peer market makers in the United States. Both have an established business history and both have funded hundreds of millions of dollars in loans. Prosper.com claims more than $306 million in funded loans, while LendingClub.com claims more than $528 million.

These market makers also set loan rates, which sounds similar to how banks operate. There is a big difference, though. When you deposit your money at the bank, as a lender you have no say in how your money is lent. The banks don’t permit you to dictate terms. So if you’re willing to accept more risk in exchange for more reward, you’re out of luck. The bank won’t offer you a higher rate for your willingness to accept more risk.

In the peer-to-peer lending market, you’re in charge. You choose the amount you want to invest (as little as $25), you choose the length of time you want to tie up your money (with a year minimum being the norm), and you choose the risk level you are willing to accept. The more risk you are willing to accept, the more income you can generate.

Opening a peer-to-peer account is as simple as opening any on-line brokerage account. Once your account is open and funded, you simply select a loan fund with the terms and risk characteristics you desire.

Conservative options – loan portfolios with very high credit scores and almost no chance of default – provide average annual returns between 6% and 8%. More aggressive options – where borrowers have lower credit scores and higher defaults – range between 9% and 12%. The riskiest portfolios offer the opportunity to capture up to 18% annually.

Once you’ve selected your loan portfolio, you’ll start receiving monthly payments just like your banker. Just as important, you’ll be earning money like your banker, and not like his depositor.