If you think that the rise in interest rates could derail the housing market, think again.

Home prices are of course a crucial piece of the puzzle for the U.S. economic recovery.

That’s because declines in the housing market reduce household wealth, and crush the growing “wealth affect.” This is of course the important increase in spending and investing that occurs based on perceived wealth.

It’s easy to see how home values influence the wealth effect.

For most Americans, our homes are our largest asset. When it's value increases, we feel wealthier. When it goes drops in value, we feel poorer. In recent years, we’ve run the gamut of wealth emotions.

A common lament these days is that rising interest rates will lower our home's values and perception of wealth. The reasoning goes as follows: Rising interest rates lead to lower home affordability and fewer home sales. This in turn leads falling home prices.

But this is simply linear thinking. And unfortunately markets aren't quite so tidy.

I'm circumspect on the perceived relationship between interest rates, home prices, and the wealth effect. I say that because the 30-year fixed-rate mortgage is up a full percentage point since late April. Yet home prices (including mine) continue to rise.

Earlier this week, Ian wrote about the booming real estate boom in Washington state, where he’s visiting family. You can read his article – Are Interest Rates Killing the Housing Recovery? – by clicking here now.

In May, the national median price of an existing home rose a very strong 8.4% to $208,000. Meanwhile, the national median price of a new home moved higher 3.7% to $263,900. What's more, persuasive forecasts from Clear Capital and Bank of America point to price gains through the rest of the year.

At the same time – and this is an important consideration – home sales volumes continue to rise.

In May, existing home sales were up 4.2%, and are expected to rise another 1.3% for June. New home sales have continued to rise as well. In May, they were up 4.8%, and they're expected to rise another 1.7% in June. Demand for housing remains strong in the face of price gains.

Sentiment is also a mitigating factor to the interest-rate threat. It too points to future gains.

Today, homebuilders are optimistic. Measures of customer traffic, current sales volume, and the outlook for single-family home sales over the next six months lifted homebuilder optimism to its highest levels in least seven years, according to the July edition of the National Association of Home Builders/Wells Fargo homebuilder sentiment index.

That said, economic growth is the most important factor when it comes to the housing recovery.

Though it doesn't always feel like it, our economy is growing and generating jobs. The June employment report shows payrolls increased by 195,000, handily beating economists' estimates. Similarly, average hourly wages rose 0.4%.

With more people working, and employees earning more, people are able and willing to spend. For some people, that means buying a new or bigger home.

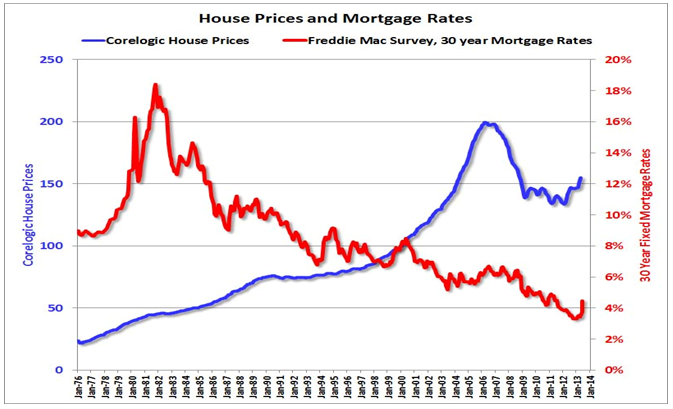

The chart below from the Calculated Risk Blog and based on Corelogic and Freddie Mac data, reveals just how tenuous the correlation between home prices and interest rates is. It suggests economic growth is the supporting pillar in the housing market.

Mortgage rates rose sharply in the late 1970s, but home prices jumped too. In the 1990s, rates were relatively flat and home prices moved higher. Then in 2007 and 2008, both mortgages rates and home prices fell. And finally, in 2013 rates have increased and so have home prices.

The correlation between home prices and mortgage lending rates is weak at best.

Home prices will continue to rise, as long as the economy continues to grow.

In short, we have a robust housing sector, marked by rising prices and rising sales volumes. Even rising interest rates won’t derail that recovery. In addition, there is a rising perception of wealth, which bodes well for consumer spending and for stock market values.

Further Reading:

Avoid $6,000 in taxes with this form – Deadline August 20th

There's one tax that's inescapable… Real Estate Tax. If you own a home, you have to pay – no matter what. Except the thing is, one group of homeowners doesn't. They haven't paid taxes in years. They're enrolled in a special program that allows them to completely pay off their real estate taxes through exclusive rebates. These rebates arrive in the form of U.S. government-backed checks. And they are available to any American, regardless of income or employment status… In fact, you can start collecting a Real Estate Tax Rebate check of up to $6,175 – Tuesday, August 20th! Click here for all the details of this unique program.