In most businesses, customers and clients usually voice their opinions on your misses, not your hits. Investment publishing is no different.

Though the High Yield Wealth portfolio has recommended a number of income investments that were successful from the get-go, by far we receive the most e-mail on the few laggards.

BGC Partners (NASDAQ: BGCP), an institutional securities trading and commercial real estate broker, tops the list.

BGC was initially recommended a year-and-a-half ago. Since then, it has traded mostly lower and has been a constant source of frustration. BGC has by far generated the most inquiry.

E-mailers most frequently want to know wants going on? But what I sense is they want to know why I continue to recommend BGC?

Though BGC has posted double-digit losses, I haven't considered selling. For one, I like the management, which is heavily invested in the business. I also like the business: securities-trading platforms for banks, hedge funds and institutional investors and commercial real estate brokering.

BGC's problems center on reduced trading volumes due largely to new capital and trading regulations imposed on banks. The good news is volumes have improved this year, and I expect they will continue to improve as the vagaries associated with the regulations are cleared and banks are more confident trading.

BGC's foray into commercial brokering in late 2011 was a savvy contrarian move into a beleaguered sector. This allowed BGC to pick up the assets of bankrupt Grubb & Ellis and Newmark Knight on the cheap.

Commercial real estate brokering has picked up the slack left by securities trading. Revenue for the segment, virtually nothing at $57 million in 2011, grew to $481 million in 2012. Operating income quadrupled to $22.9 million from $5.7 million.

Management recently proved it was equally savvy at selling. This past Monday, BGC announced it was selling its eSpeed bond unit, an electronic Treasury trading platform, to NASDAQ OMX Group (NASDAQ: NDAQ) for $750 million in cash. The total could rise to $1.2 billion if certain sales goals are met.

OMX is actually paying more for eSpeed than the entire market cap of BGC, which was around $600 million before the acquisition was announced. In short, OMX is paying a 7.5 multiple for a business segment that generated around $100 million in revenue last year. What's more, BGC will still retain all of its voice, hybrid, and fully electronic trading, market data, and software businesses.

After reading the terms of the deal, I was hardly surprised BGC shares soared over 48%.

As for the cash proceeds from the eSpeed sale, CEO Howard Lutnick declined to specify how the cash will be used, responding “nothing is off the table.” Given management's proven ability to buy cheap and sell dear, I expect the cash will be used to create more investor value.

BGC's price recovery provides two valuable investing lessons.

First, when you have faith in a company and its management, you don't sell just because of a temporary bad spell. The people who manage BGC also manage Cantor Fitzgerald, a trading firm that lost two-thirds of its employees on September 11, 2001. Cantor Fitzgerald recovered completely from that devastating blow. I was confident that it was only a matter of time before BGC would return to form as well.

The second lesson is investors should stay invested during the dark days. When the going gets tough, I'm invariably asked, are you getting out? (This is really the disguised question, should I get out?)

I always answer, ”no,” because you have to be in the market to be a successful income investor. Cash doesn't generate a return; income-generating investments – the kind that comprise the High Yield Wealth portfolio – do.

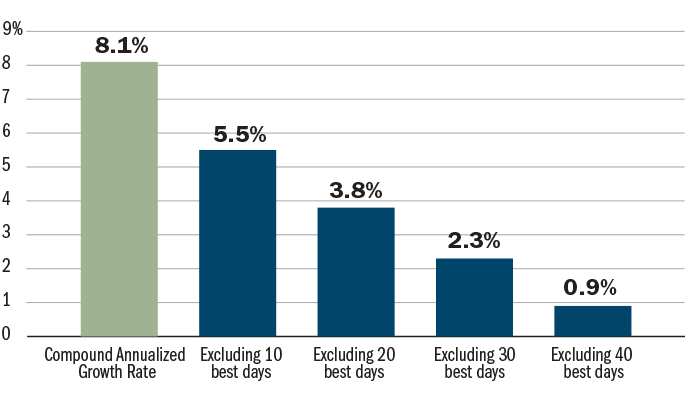

The problem is, I don't know when investment return will materialize. What's more, I only need to miss a few strong-advance days before long-term return suffers.

The chart below reveals the importance of being invested and how returns are hurt when investors are sidelined during stock-price rallies.

S&P 500 Returns

BGC proves that staying the course and maintaining faith in your analysis will pay off over the long haul. I'm in BGC for the long haul, and I expect more rewards lie ahead.

For the past couple months, I've been recommending that High Yield Wealth readers add to their BGC positions in order to lower their cost basis and capture additional yield. It's satisfying to know that those who bought BGC shares in spite of recent uncertainty have been amply rewarded.