At the High Yield Wealth newsletter, we have two mandates: income and investments that have merit individually and within a portfolio context.

On the former – income – the High Yield Wealth portfolio yields 7.2% on a cost-basis measure. I expect that yield to rise, as many of the portfolio investments continue to raise their payouts.

Rising payouts nearly always lead to price appreciation over time.

The investments must also contribute within a portfolio context, i.e., they must reduce portfolio risk.

I am bullish on business development corporations (BDCs), but I'm not going to overweight the portfolio with BDC investments. I say that because correlations between investments matters. Investments that are lowly correlated reduce risk, but not return potential.

Sure, the BDC sector outlook looks promising, particularly for Ares Capital Corp. (NASDAQ: ARCC), Prospect Capital Corp. (NASDAQ: PSEC) and Medallion Financial (NASDAQ: TAXI). But I would never hold a portfolio comprising only BDC stocks. It would be too volatile and risky, even though the aforementioned BDCs are reliable, high-yield dividend payers and growers.

Which brings me to gold. I like gold because it's a risk-reducing, portfolio-diversifying asset. It's also been a strong-performing asset over the past decade – up nearly 400%.

What's more, it's been reliable. In 2008, when the major U.S. indices plummeted 37% (and more into early 2009), gold returned nearly 6%.

On its own, gold has obviously been an exceptional investment. But it’s also been an exceptional investment within a portfolio context. That is, it has provided return while reducing portfolio risk. Gold has, in essence, been a free lunch.

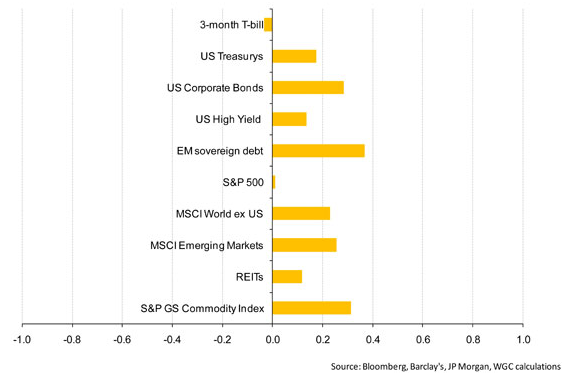

The chart below shows gold's historical correlation with other assets: the lower the correlation (close to zero and negative), the better. Gold has provided exceptional return on dollars invested, while also significantly reducing the overall risk profile of an investment portfolio.

Gold's Correlation with Other Assets

I've fielded quite a few questions on gold over the past month, typically asking whether gold is still worthwhile to add to a portfolio. I understand the concerns. Many investors have been put off by recent volatility, which has been particularly pronounced over the past three months, as shown below.

Three-Month Gold Chart

Despite the recent spike in volatility, I still like gold. I obviously like its portfolio diversification benefits, as discussed above. Low correlation levels in the price of gold compared to other assets is a primary factor in enhancing overall portfolio performance. You don't have to be bullish or bearish on gold to get the benefit; you just have to own gold.

Past performance has also been something to crow about. Over the past 10 years, gold has significantly outperformed all equity markets. In fact, it has outperformed the S&P 500 by a three-to-one margin.

That said, past is not always prologue. Except this time I think it is, because gold is also private money. Gold is a store of value and a back-up medium of exchange. Gold is an insurance policy against reckless money printing.

Our Federal Reserve, quite frankly, is reckless. It has more than tripled the base money supply over the past three years, and it continues to expand the base by $40 billion a month. Both moves are unprecedented.

What's more, each new dollar diminishes the purchasing power of all outstanding dollars. I see no reason why gold shouldn't continue to hold its purchasing power and appreciate in dollar terms.

I do have one problem with gold: it isn't a cash-generating asset. It doesn't provide cash flow, and that's a problem at High Yield Wealth. That said, the High Yield Wealth portfolio has a gold component. I've found a gold investment that offers a high yield – at 10.5% as I write – and monthly income, so it's suitable for income investors.

The point I want to emphasize is that through the right investment vehicle, gold can be structured to meet every investor’s needs. And that includes the needs of income investors at High Yield Wealth who also want a portfolio-diversifying asset.