You probably don’t need me to remind you that the “fiscal cliff” is fast approaching.

If Congress is unable to settle several key tax issues by year’s end, $540 billion could potentially be taken out of our wallets and put into the government’s coffers. Is it time to hit the panic button?

Congress’s own financial analysts have warned that going over the fiscal cliff would almost certainly trigger a recession in 2013. And congressionally-appointed analysts are always accurate, right?

If that wasn’t enough, Citigroup recently issued a dire warning about the U.S. and global economies falling off the fiscal cliff. Citi analysts stated the economy would sink into another recession, leading to a sharp decline in the stock market, oil prices dropping by roughly $20, a potential 5%+ depreciation in the dollar, and unemployment rising to a minimum of 9.5% through 2014 (it’s 8.1% now).

As self-directed investors, what does all of this financial chicanery mean for you and me?

Are we just witnessing politicians being politicians? Is the media overhyping the situation? Should we really be concerned about our long-term investments in the market?

One thing is certain. If we avoid the fiscal cliff (which I think we will), rest assured that we will face tax hikes on capital gains and dividends because a large part of the inevitable tax increase – approximately $250 billion – will come from Bush tax cuts expiring.

As it stands now, dividends get preferential tax treatment. The highest tax you pay on a traditional dividend stock is 15%, regardless of your income tax bracket. The same applies to long-term capital gains. The low tax rates make dividend-paying stocks and dividend income extremely attractive to self-directed investors.

So what happens when or if Congress decides to change the current rate on dividends and long-term capital gains to the same level as ordinary income?

History offers some insight.

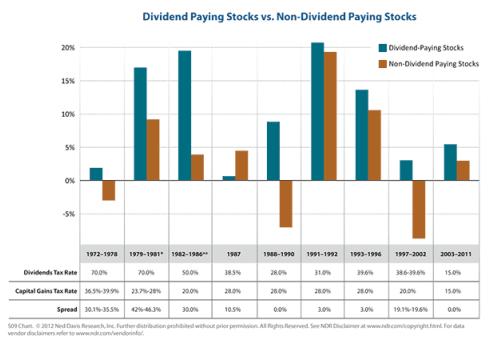

The chart below from Ned Davis Research looks at previous periods when dividend tax rates were significantly higher than they are now. Moreover, it shows periods when the dividend tax rate differed from a capital gains tax, a situation that we could face going forward.

Don’t get me wrong, lower dividend and capital gains taxes are a benefit to all investors. But again, on a historical basis, lower taxes did not have an overwhelming effect on the performance of dividend-paying stocks. In fact, returns on dividend-paying stocks were actually higher during periods of higher taxes on dividend income.

So what should we expect?

With taxes on capital gains and dividends likely headed higher, it would not be surprising to see a dip in the market over the intermediate term. A large wave of investors could cash out large gains before the 15% rate expires.

However, this could afford another wonderful opportunity to ramp up your allocation to dividend stocks. Either way, as long-term investors we should not concern ourselves with these unavoidable bumps in the road. They will always exist in the marketplace.

All we can do as self-directed investors are look for high-quality companies that share their success with shareholders, and that are able to increase their dividends by increasing free cash flow. This should be an integral part of any investor’s portfolio, regardless of the tax rate we pay on dividends. Remember, it’s the underlying business models of such companies are the true driving factor behind performance. Compounded investment income – not style, sector or market capitalization – is the leading factor driving total returns.

At the end of the day, when the dividend tax rate changes – and it eventually will – income from dividends will be no more disadvantaged than income from bonds. And dividends offer more opportunity for growth. Just ignore the constant stream of noise that is being thrown at us on a daily basis. Ultimately, we all know dividends will remain a sound investment over the long term … no matter how Congress finally decides to act.

Stay the course.

Kindest,

Andy Crowder

Editor and Chief Options Strategist