The question is repeatedly pondered: What is the secret to Warren Buffett's breathtaking investing success?

There is no shortage of commentators weighing in on the subject. One recurring anecdote, which has really digressed to cliche at this point, is that Buffet buys "great companies at a fair price."

Sounds great, but what does that really mean? How do you determine if a great company is fairly priced, or if it's a great company to begin with? Are greatness and fairness based on a price-to-earnings multiple combined with sales and earnings growth? Maybe return on equity; or perhaps growth in book value? Or is it some other combination of variables?

Theories can get complicated, but I don't think they need be. This passage from Buffett's letter to investors in 2010 says it all about company greatness from the investors' perspective:

Coca-Cola (NYSE: KO) paid us $88 million in 1995, the year after we finished purchasing the stock. Every year since, Coke has increased its dividend. In 2011, we will almost certainly receive $376 million from Coke, up $24 million from last year. Within ten years, I would expect that $376 million to double. By the end of that period, I wouldn't be surprised to see our share of Coke's annual earnings exceed 100% of what we paid for the investment.

Greatness, I believe, is revealed in Buffett's dividend-growth strategy – buying established brand-name companies that continually hike their dividend: Coca-Cola pays hundreds of millions of dollars to Berkshire Hathaway (NYSEP BRK.a) annually, but it's not the only company to do so. Other dividend growers help to swell Berkshire's coffers: American Express (NYSE: AXP) adds $109 million a year and Proctor & Gamble (NYSE: PG) contributes $150 million at the going dividend rate.

I view these dividend growers as the corpus of Buffett's tremendous wealth and the funding source of many of his other investments.

I've long been sold on the power to generate wealth by investing in a swelling stream of dividends. In fact, I've carved out an entire space for dividend-growth stocks in the High Yield Wealth portfolio.

McDonald's (NYSE: MCD) is one of those stocks. In fact, McDonald's was the top performer in the High Yield Wealth portfolio this year, posting a 15% dividend increase on top of a 30% increase in share price. McDonald's has a long history – 35 years – of increasing its dividends annually.

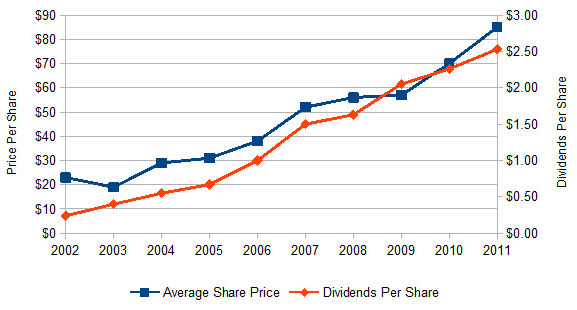

There is a systematic, wealth-compounding effect that occurs when dividend payouts grow, even if the payout isn't particularly enticing at the time of purchase. Let's consider McDonald's: the company's average share price was around $6.00 (split adjusted) in 1991. At the time, McDonald's was paying $0.09 in dividends annually, which translates to a 1.5% yield.

A 1.5% yield doesn't sound like much, but let's fast forward 20 years. Today, your $6.00 investment is paying $2.80 annually, based on McDonald's latest dividend increase. That means your original $6.00 investment is yielding 46% annually. In other words, McDonald's is paying you almost half your purchase price in dividends each year.

If McDonald's were to increase its dividend 10% annually (which is actually below the 10-year rate of 19%), in eight years, you'd be receiving annual dividends that equal the cost of your initial investment. Welcome to Warren's world!

Of course, your $6 initial investment isn't going to stay at $6. Investors will bid the share price higher. That's been the case with McDonald's; as the dividend rises, so too does McDonald's share price.

Dividend-growth investing is a wonderfully straightforward strategy for accumulating wealth over time – that is, if you know how to implement the strategy.

Like Buffett, I seek dividend growers with leading positions in their respective industries that have a long record of increasing revenue, earnings, and dividends annually and that aren't trading at unreasonable earnings multiples. Over the past year, I've added a few of these stocks to the High Yield Wealth portfolio. In 2012, I look forward to adding a few more.

Stephen Mauzy, CFA

Research Analyst

High Yield Wealth