Bernanke doesn’t fear inflation. And neither do I.

Inflation isn’t a near-term threat and hyperinflation won’t happen any time soon.

Not only has CPI not gone above 4% in over a year, it hasn’t marched above 3% over the past 12 months. Furthermore, CPI data last week showed a 0.6% rise in September. There is not enough evidence suggesting CPI will dramatically spike higher within the next few years.

Though the Fed has increased its balance sheet to a level previously thought insurmountable, inflation remains low.

Quantitative easing is not igniting inflation in the way that many have deemed probable. The program is four years old and CPI hasn’t budged throughout its implementation.

But gold continues to march higher even though inflation is subdued. And I think the gold ascent has further to go.

Despite the lack of CPI growth, the yellow metal should continue its trajectory if GDP stays above nominal bond rates.

Bridgewater (a top investment company) research explains that the relationship between GDP and interest rates is a major factor between good and painful deleveraging. We’ll also see how this is bullish for gold later on.

Recall (here) that deleveragings need more than one pill to fix. Quantitative easing provides some relief, but more help will be necessary.

In order to maneuver through the deleveraging process successfully, it takes a combination of debt restructurings, wealth distributions, austerity, increasing the money supply, and businesses lowering breakeven basis. And nominal interest rates need to be below economic growth rates.

To its dismay, the Fed has less control over deleveragings than it would prefer. The Fed cannot control wealth distribution (higher taxes), austerity (spending cutbacks) and lowering the breakeven basis for businesses (increasing efficiency and firing workers). Through quantitative easing, the Fed is trying to control money supply, debt restructurings and the interest rate premium over GDP – with the latter being extremely important.

Good deleveragings unfold when GDP growth stays above bond yields, which is why the Fed is buying bonds from the open market (quantitative easing). It must keep nominal bond rates extremely low because GDP growth has been anemic. As GDP improves, the Fed can be tighter (hawkish) with bond yields.

But the real key to the deleveraging equation is not just keeping bond rates low, it’s keeping the rate below GDP growth.

This has proven more difficult lately because annual GDP growth has struggled to stay above 3%. And most analysts predict GDP will drop below 2.4% next year. If interest rates and GDP don’t drop in tandem, investors will have reason for fear.

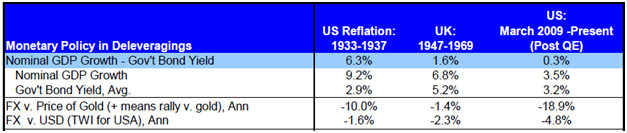

This table shows what happens when interest rates are above GDP rates during a deleveraging. The relationship explains why Japan’s economy remains sluggish more than 20 years later.

Present indicates through 2011, The World Index (TWI), U.S. Dollar (USD), foreign exchange (FX)

Present indicates through 2011, The World Index (TWI), U.S. Dollar (USD), foreign exchange (FX)

The above deleveraging time frames were some of the worst periods for investors, consumers and businesses. These examples stress how painful a recovery period can be when GDP growth is below bond rates during deleveragings. These are also great times for the domestic currency.

However, the recovery process is not nearly as trying for investors, consumers and businesses when GDP is above bond rates. In fact, this has typically been an excellent period for stocks and commodities investors.

This table shows what happens when interest rates are below GDP rates. Investors have typically flourished during these periods. The impact on the local currency was also small, although some of its vale tended to be lost against other currencies.

Present indicates through 2011, The World Index (TWI), U.S. Dollar (USD)

Present indicates through 2011, The World Index (TWI), U.S. Dollar (USD)

Deleveragings are tough periods to manage, but there are solutions available that have proven to work. One of the less painful ways to reflate appears to involve keeping GDP above bond rates.

Ben Bernanke recently explained why GDP is important so much better than I ever could, “The crisis and recession have led to very low interest rates, it is true, but these events have also destroyed jobs, hamstrung economic growth, and led to sharp declines in the values of many homes and businesses. The best and most comprehensive solution is to find ways to a stronger economy. Only a strong economy can create higher asset values and sustainably good returns for savers. And only a strong economy will allow people who need jobs to find them.”

You have it from the horse’s mouth – Bernanke wants GDP growth. This is his primary objective. And he wants to achieve it by keeping interest rates low (making open market purchases).

This is fantastic news for investors holding gold.

Quantitative easing takes a toll on savers, but it raises the values of other assets, such as gold. Gold tends to rise during deleveragings, and it performs incredibly well when GDP is above bond yields.

This means that gold should continue to climb higher as long as GDP growth stays above 3%, which is roughly what bonds yield.

Through quantitative easing the Fed is keeping interest rates low and targeting GDP. This combination should result in a GDP rate that exceeds bonds. When that combination occurs, gold tends to shine.