It's every miner for himself right now in the gold and silver mining industry; a total rout. These stocks are getting trampled over as investors flee the sector with reckless abandon. To fully understand what to expect next we need look at the clearest evidence on the table – then project what's likely to occur.

If you don't understand where we've been (and why), you'll never be ready for where we're going, how we'll get there and how to play it.

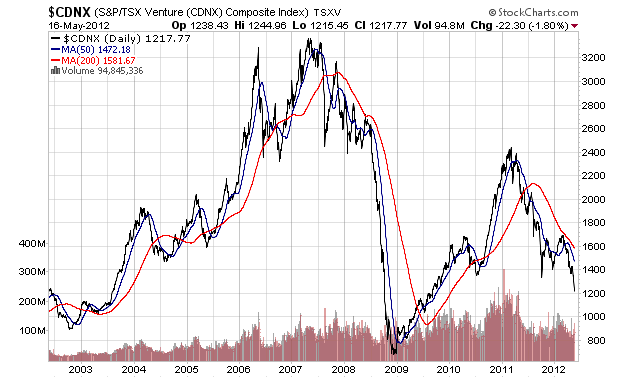

Right now, the gold bears are winning the battle as the TSX Venture Index just cracked through 1400, the last remaining support level before the lows of late 2008.

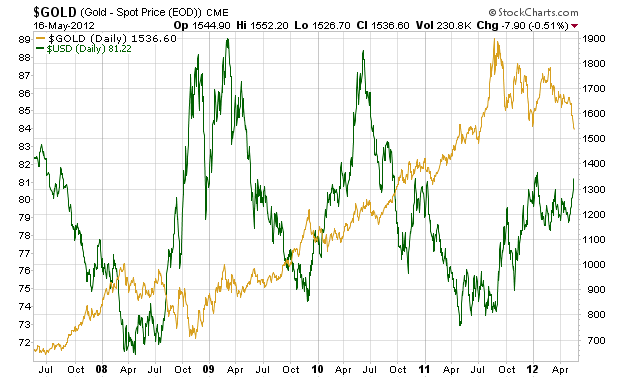

The junior gold miners are naturally influenced by the falling price of gold – which is in part related to the recent rally in the dollar as fears of a European banking crisis resurface.

The retreat in gold is a story unto itself, and all miners are feeling the pain. But it's clearly the juniors that are in the greatest danger. Some of these companies could cease to exist soon – unless they are bought out.

With no revenues to support ongoing exploration efforts, let alone pay salaries, these companies can only look to the equity markets to raise funds. No bank is going to loan them money at this stage. And this means exponential shareholder dilution will happen as share prices fall and companies get diminishing returns on equity offerings.

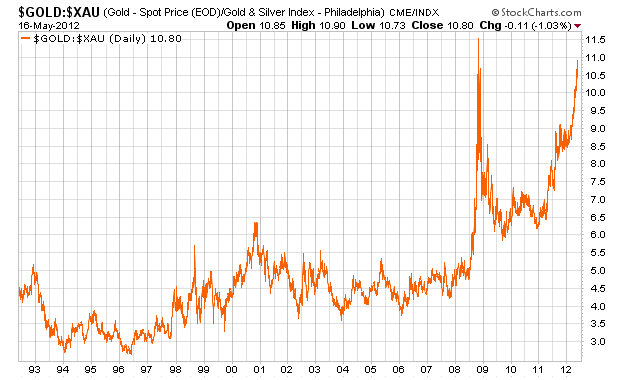

Stepping back from the juniors to look at the broader-based mining sector as measured by the Philadelphia Gold and Silver Index (XAU) – an index of the biggest and most stable miners such as Goldcorp (NYSE: GG) and Barrick Gold (NYSE: ABX) – it becomes apparent that we are approaching historical extremes in terms of the relative value of gold and miners.

The following chart divides the XAU into the price of gold over the last 20 years to show how many units of XAU can be purchased with an ounce of gold. The trailing 20-year average is between 4 and 5, but right now we are closer to 11. This ratio hasn't been at such extremes since late 2008.

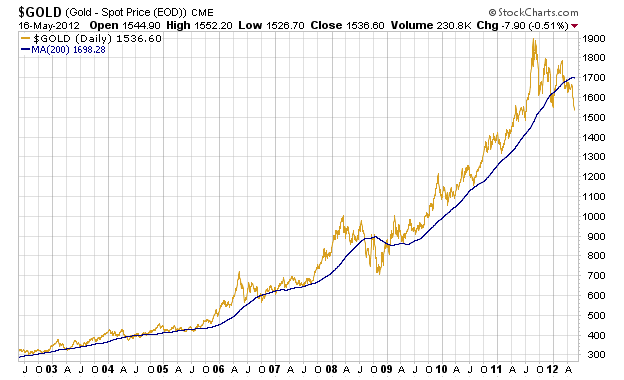

The only way for this ratio to come back into its historical range is if gold mining stocks rise or if the price of gold falls, meaning that an ounce of gold would buy fewer shares of the XAU. Again, we have to go back to 2008 to see what happened to the price of gold to bring this ratio down. The result then was that gold cracked its 200-day moving average with conviction, as it has recently, and retreated 30% from its high of around 1100.

A similar correction today would mean we're looking at gold falling from its 2011 high of $1900 an ounce to around $1330. At that point, based on recent history, it'll be time to aggressively buy gold stocks.

I think it's still too early to accurately predict when, and how, this will ultimately play out. But we can build a game plan to potentially make huge profits in this sector if we can be even close to right.

One of the signals that things are turning around will be when majors and mid-tier producers start buying up juniors. For some producers this will be the best way they can build their pipelines – especially as costs to build new mines have risen. And for many juniors, selling will be their only viable option to return money to shareholders, and possibly find new jobs for executives and employees.

Trying to figure out what juniors will get bought out is exceptionally difficult. If you go this route, I'd look for those with low-cost mines with long life expectancy, and juniors with well-funded operators paying for the exploration on their properties. That's a lot of work, and requires a lot of speculation.

A safer route is to buy juniors that have new production-generating revenues now, and which are helping them build a capital base to fund ongoing operations. I believe these stocks offer the best reward vs. risk profile in the sector.

The rout in the mining sector isn't going to end in one day. But we will see capitulation at some point. History suggests that we are getting close – all else being equal. Look for signs of majors buying juniors as one signal. And play the trend by buying those with production growth to get the best reward, with the least downside risk.