I’ve long been a proponent of timber as an asset class. It’s a great way to de-risk your portfolio with a timeless asset because it’s generally uncorrelated with stocks, bonds – and it’s positively correlated with inflation.

So it’s basically the best of both worlds as an investment.

Timber has also crushed the S&P 500 on average. According to CNBC, "From 1987 through 2007, timber delivered an average annual return of 15.8 percent…"

And today, wood prices are in a crisis. According to Dr. Jacobson of the Penn State College of Agricultural Sciences Extension, things aren’t looking so good for timber.

In his Q3 2011 report published a few weeks ago, he wrote:

"This may be the worst I’ve seen average stumpage prices since I’ve been reporting. The Southeast remains the only bright spot. The Northwest and Southwest are not only suffering from the poor economy, but the rapidly expanding natural gas industry is taking jobs and income away from the forest sector."

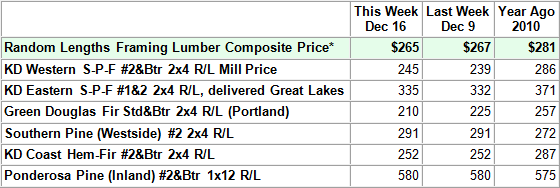

Dr. Jacobson’s assertion is backed by this table showing recent lumber prices compared with prices a year ago:

*Courtesy of the WoodWire

Nearly every type of domestic wood is cheaper than it was a year ago. And remember, a year ago, the housing market was still in freefall.

But according to a recent report from everyone’s favorite investment bank, Goldman Sachs (NYSE: GS), the bottom for housing is finally within view.

From The Wall Street Journal story on Goldman’s report:

"Goldman’s analysts, Hui Shan and Sven Jari Stehn, project that the national S&P/Case-Shiller home price index has 2.5% to fall before it hits bottom next summer [of 2012]."

I don’t know if Goldman is exactly right, but it seems that housing is probably close to a bottom, and that regional strength in some markets will likely boost timber demand.

So that’s another bullish trend for timber and lumber prices.

How can you play this trend as an investor?

There are lots of timber REITs out there. There are a few timber ETFs and some straight timber land companies.

But I’m not a fan of most of them. The timber ETFs do a terrible job of tracking timber. Most of the REITs don’t track timber very well either – and they have the added benefit of being small and volatile.

I would suggest buying actual timber land, but that’s a tall order for most regular investors.

But your second best bet is to buy my favorite timber land company.

Unfortunately, my favorite publicly traded company is likely to be added to next month’s addition of our paid research service on high-dividend paying investments called High Yield Wealth – and the product’s editor (my boss, Ian Wyatt) asked me not to mention this company in this free publication.

Not to be a transparent pitch-man for the product, but a trial subscription only costs $49 a year – and that cost comes with a 100% money back guarantee if you’re at all displeased. So if you are interested, you can try out High Yield Wealth for yourself, and then cancel at the end of the trial period if you’d like.

Of course, I hope you’ll remain a subscriber, and I believe that you’ll be pleased with the research, so I’m not too worried about cancellations.

To read more about High Yield Wealth, click here.